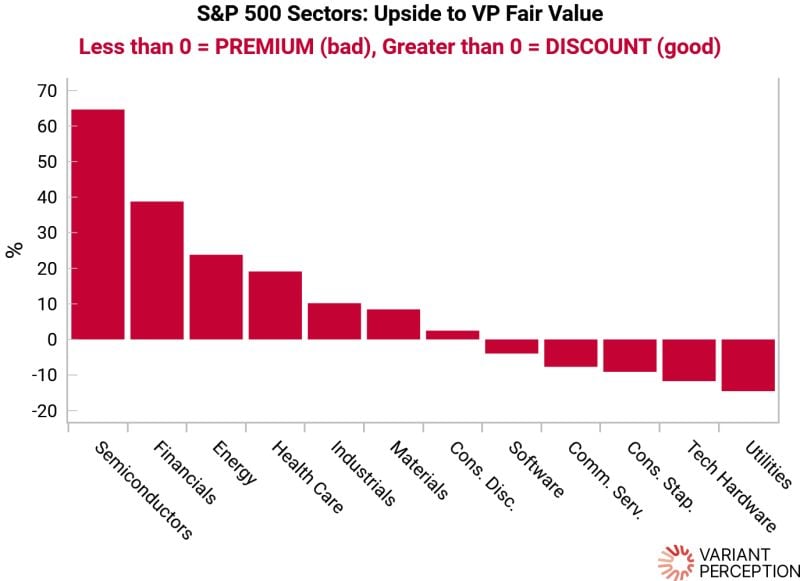

A. CHART OF THE WEEK

Semiconductors, financials, energy and healthcare remain favored, with the most upside to our estimates of fair value.

***

C. RESEARCH

Navigating Complacency and Narrowing Breadth - Macro Snapshot - June 1

- All 3 legs of our post-Iran roadmap are still intact with a US manufacturing rebound, continued “jobless” growth, and the upcoming SpaceX IPO potentially marking the speculative mania phase of this cycle.

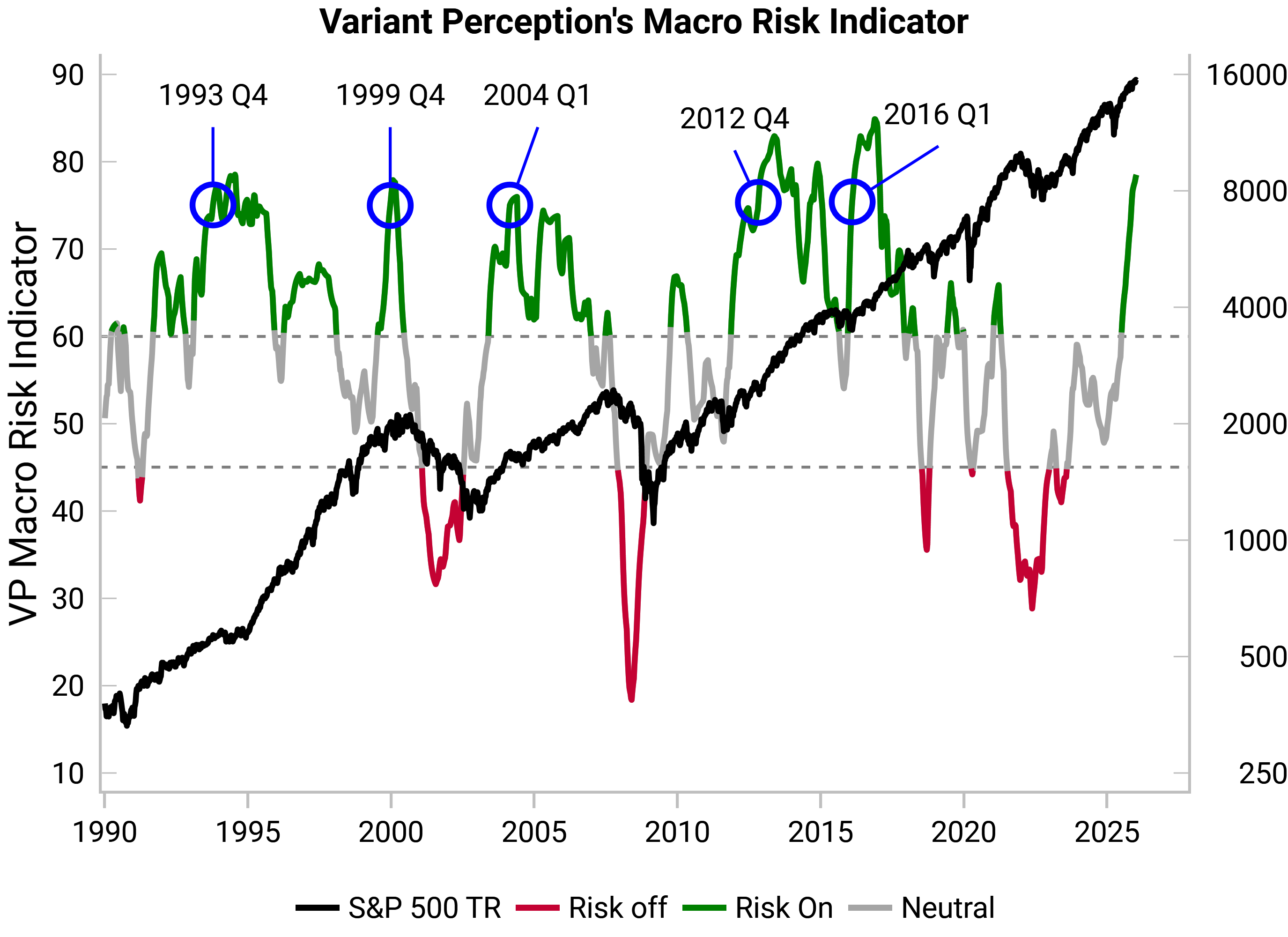

- Our Macro Risk Indicator remains “risk-on” for now, but there are more signs of investor complacency. Investors should consider adding energy exposure as well as going long index volatility to take advantage of the very low implied correlations.

- Major tops are characterized by narrow market breadth alongside monetary policy tightening and liquidity headwinds. The potential saving grace today is that US inflation may be transitory.

***

Summary

- Cyclical Asset Allocation: Macro Risk Indicator remains risk on, but investor complacency now more prevalent

- 2026 Roadmap Update: Equity market breadth holding up, transitory inflation can be looked through, manufacturing rebound continues, “jobless” growth persists

- Policy Stimulus: G3 stimulus impulse turns negative, a risk that could build as 2H26 goes on

- Sector Allocation: OW: Semis, Energy, Financials, Healthcare; UW: Consumer, Non-Semi Tech

- Equity: Earnings leading indicator rolling over as animal spirits start to surge

- Fixed Income: LPPL exhaustion on yield surge, still skeptical of 2022 repeat

- FX: Cyclical tailwinds persist for stronger USD, politics the bearish structural factor

- Commodities: Cyclical macro outlook more neutral, goldminers offer value

Other Insights

Practical insights on allocation, diversification, and risk tolerance—combining behavioral, liquidity, and structural perspectives.

Contact Us

Stay Connected

Our research is built for investors who need timely, repeatable insights.