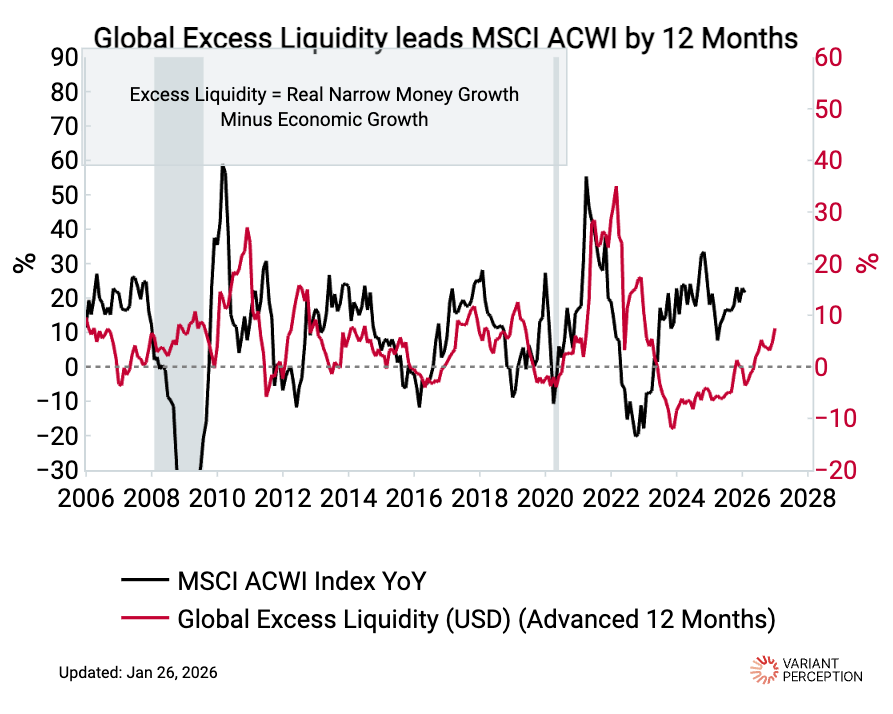

Chart of the Week

***

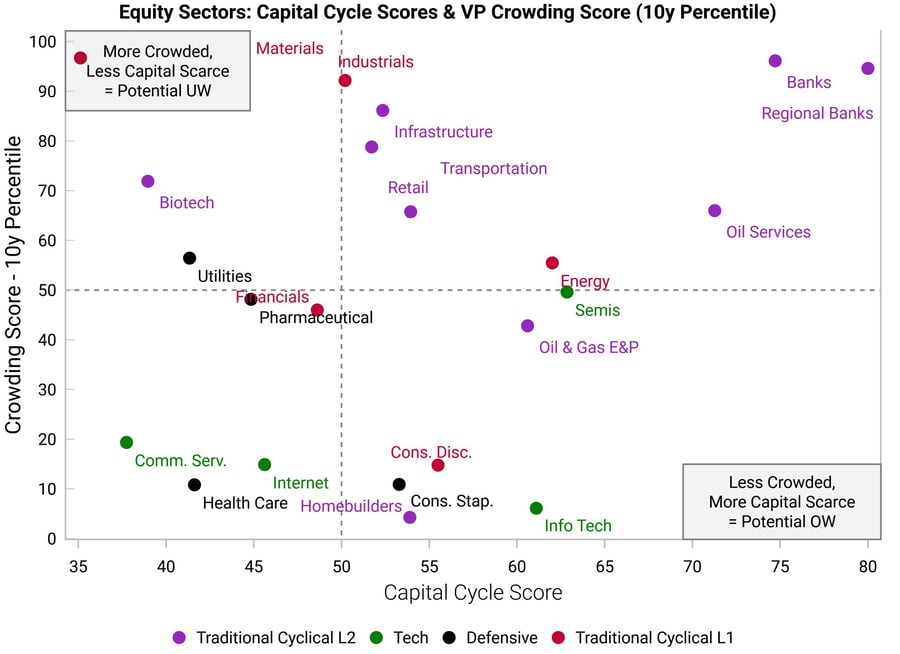

The best time to invest is when a sector is uncrowded and capital scarce. Over the past three months, these shifts stand out.

(1) Crowded Cyclicals

Crowding has risen sharply in cyclicals — Banks, Industrials, and Materials. The “reflation” trade has quickly become consensus. This is not itself a reason to sell. But further upside is more reliant on improving economic data.

(2) Tech Anomaly

Surprisingly, tech remains relatively unloved. Its capital cycle score is till favourable. Marginal returns on investment are holding up and exceed the cost of capital. This keeps tech attractive for growth at reasonable valuations.

***

Research This Week

Japan: The “impossible trinity” mechanism + what to watch to buy the yen

The Japan “doom loop” narrative has built momentum over the past six months, as the yen and JGB selloff has become disorderly. We see some validity to this narrative given Takaichi’s fiscal largesse, but the underlying mechanism is that policymakers are being pushed back into Japan’s “impossible trinity” problem.

Basically, Japan cannot have both exchange rate stability and such a slow pace of monetary policy normalization.

Our best guess is that USDJPY goes higher first (i.e., weaker yen) before Japanese policymakers will be forced to take action to exit the “impossible trinity” later this year.

Where “push” and “pull” align - Jan. EM/DM Leading Indicator Watch

Cyclical macro tailwinds are strong, and our Macro Risk Indicator remains in “risk on” territory.

Ample liquidity conditions still favor EM assets over DM assets, and we see opportunities in ex-US assets that go beyond the “sell America” narrative and are attractive on their own merits.

This month, we take profit on our short Canadian 10y bonds trade and add a UK SONIA trade to benefit from more cuts being priced in beyond September 2026. We also retain long Brazil equities & bonds; long Indonesian equities & long IDR vs short USD; long NZD vs short EUR; and long KRW vs short USD.

***

***

Summary

- UK: Stagflationary again => more cuts later, not priced into SONIA curve

- Japan: “Impossible trinity” back in play => yen weaker before it gets stronger

- France: Stable LEIs, equities are outperformance candidate within DM

- Canada: Take profit on short 10y bond trade as recession risks priced out

- Brazil: Disinflation + signs of growth recovery => stay bullish

- Mexico: Growth headwinds persist, MXN poised for weakness before USMCA

- Indonesia: Political risks vs improving macro set up

- South Korea: Rising growth and inflation to prompt hawkish BoK => long KRW vs short USD

Other Insights

Practical insights on allocation, diversification, and risk tolerance—combining behavioral, liquidity, and structural perspectives.

Stay Connected

Our research is built for investors who need timely, repeatable insights.