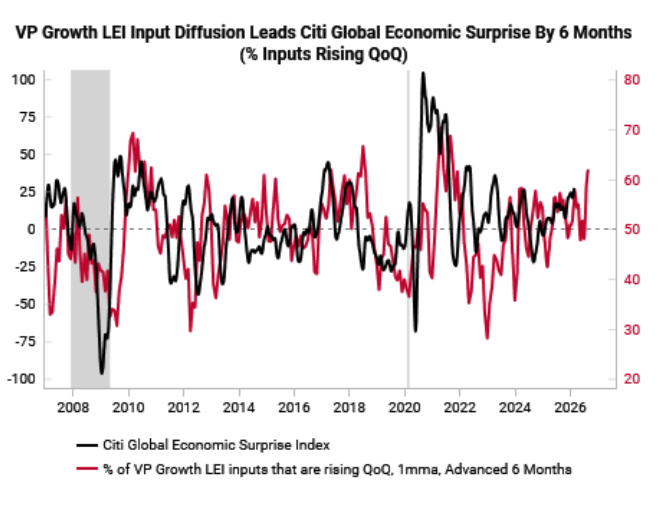

Chart of the Week

The Euro’s breadth vs other G10 currencies is breaking down.

.png)

***

Research This Week

Optimism is consensus, but that’s ok for now - Jan. G3 Leading Indicator Watch | [Watch Discussion]

- US: Growth remains resilient with moderate upside risks on the back of a renewed fiscal impulse, continued Fed easing, and early signs of a manufacturing rebound.

- China: Our growth impulse leading indicator has rolled over, while liquidity tailwinds are fading at the margin. We still like Chinese tech equities.

- Eurozone: Cyclical leading indicators continue to recover. However fiscal optimism is already consensus. We are shifting our short EUR exposure to long NZD.

US

- Growth: Resilient growth, fiscal drag to reverse in 2026

- Labor: Coincident labor data still holding up, “jobless recovery” playbook intact

- Inflation: Sticky inflation to be offset by housing disinflation and soft labor markets

- Manufacturing: Manufacturing rebound still on the cards as tailwinds build

China

- Growth impulse leading indicator now neutral as liquidity tailwinds fade

- Not yet time to fade RMB strength, time to buy Chinese tech equities

Eurozone

- Cyclical leading indicators still recovering, but fiscal optimism is consensus

- Inflation stubborn, shift short EUR exposure to long NZD

Global Macro Update: Short EURNZD, Short USDKRW, Long KWEB

We are refining and adding to our Global Macro Trade Ideas aligned with our 2026 Themes following recent price action and tactical model triggers. These include:

- Switch to long NZD vs short EUR

- Add long KRW vs short USD

- Add long China internet equities (KWEB)

Other Insights

Practical insights on allocation, diversification, and risk tolerance—combining behavioral, liquidity, and structural perspectives.

Contact Us

Stay Connected

Our research is built for investors who need timely, repeatable insights.