***

Transitory US inflation vs fragile Eurozone growth - May G3 LIW

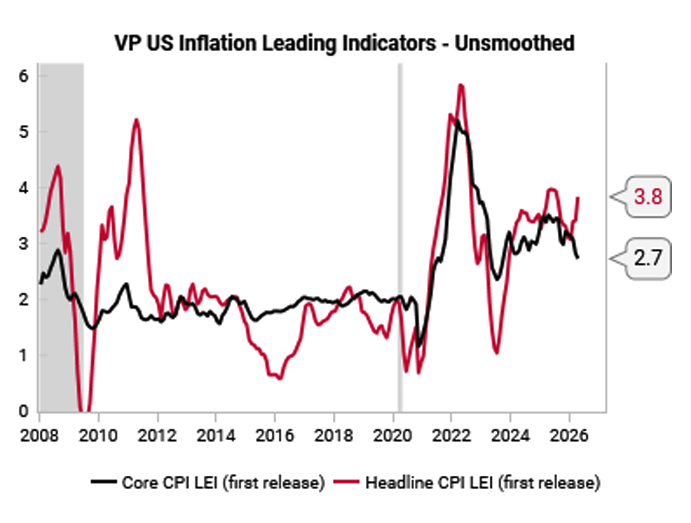

- There is a notable split among the G3. US growth remains resilient, and while US headline CPI has risen due to the Iran conflict, core inflation pressures are muted and likely transitory.

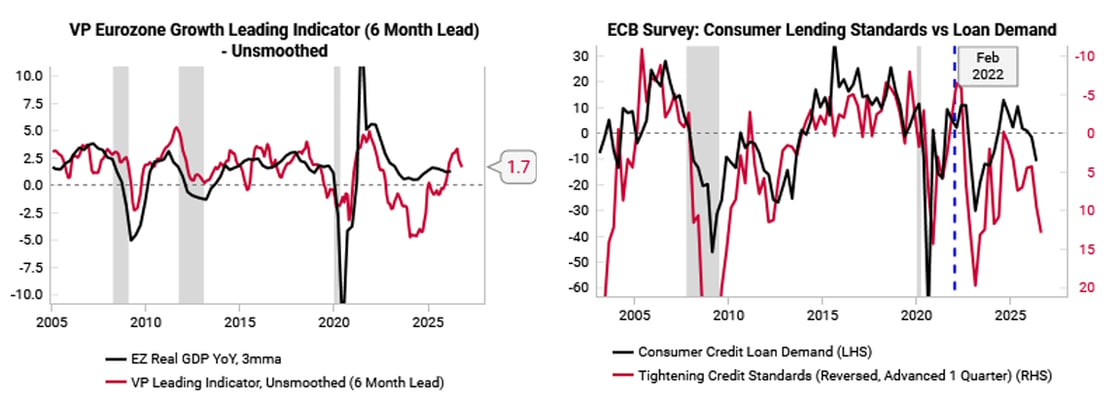

- In contrast, Eurozone leading indicators are deteriorating in unison, while the ECB is at risk of a policy error due to its price stability mandate.

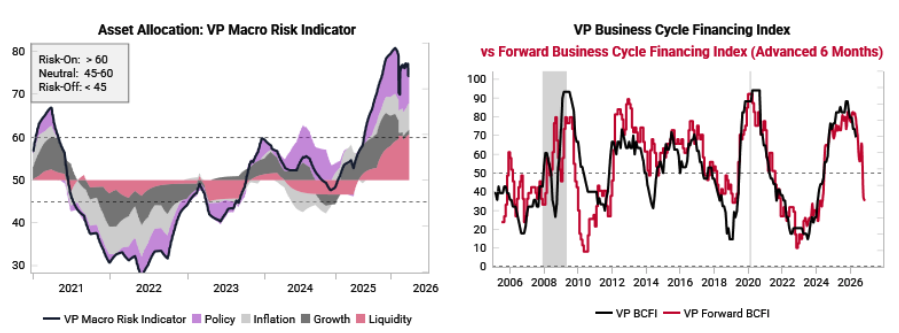

- Major global growth decelerations typically require both hard economic data and financial markets to deteriorate simultaneously to create self-reinforcing feedback loops. This condition is not met today, as credit spreads remain tight.

- The primary second-order risk resulting from Iran is that global central banks tighten policy in sync in 2H26. A synchronized global tightening cycle could drive a simultaneous deterioration in hard economic data and a drawdown in risk assets.

***

***

Summary

- Global: Global growth risks balanced with slight negative bias, G3 economic surprises diverge

US

- Growth: Steady growth outlook: resilient manufacturing, softening services

- Consumer: Muted real disposable income growth, headwinds starting to build

- Labor: Not yet recessionary, not yet inflationary

- Inflation: Headline inflation mechanically higher, but core inflation pressures are mute.

China

- Growth: Outlook muted, policymakers remain reluctant on stimulus for households

- Inflation: Transitory supply-driven inflation, underlying trend remains disinflationary

Europe

- Growth: Notable downside risks, as leading indicators deteriorate in unison

- Inflation: Notable upside risks, as ECB is stuck and at risk of 2011-style policy error

***

Other Insights

Practical insights on allocation, diversification, and risk tolerance—combining behavioral, liquidity, and structural perspectives.

Contact Us

Stay Connected

Our research is built for investors who need timely, repeatable insights.