“Invert, always invert” - Charlie Munger.

If you measure the height of every adult male in America, you will get a near perfect Bell Curve. Most people are average height; very few are giants.

But the stock market does not look like a Bell Curve. It looks like a Power Law.

Academic research shows that the vast majority of stocks are statistically "losers." In fact, the majority stocks have negative lifetime returns. The data is truly stark.

Since 1926, the S&P 500 has returned +10.3% annualized, but the average of all single stock returns is -9.7% while the median of all single stock returns is -0.8%. This means a minority of stocks account for almost all of the returns of the overall stock market.

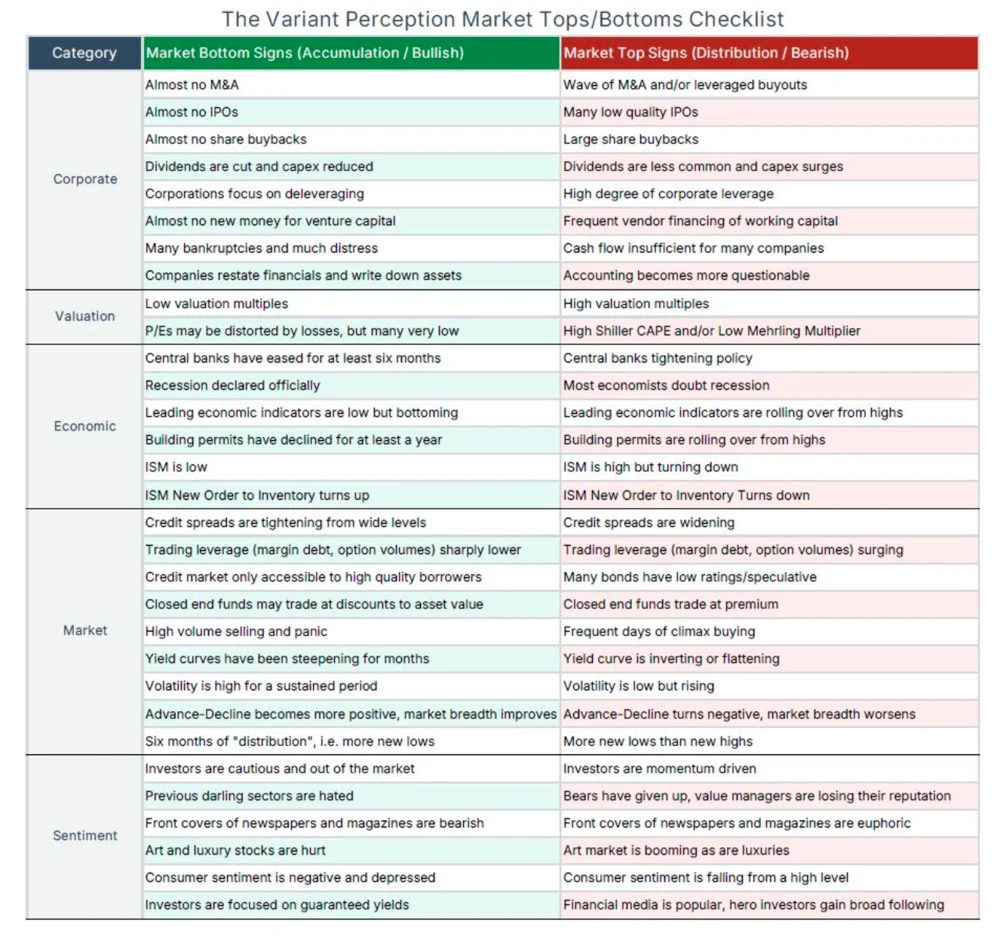

.png)

This creates a dilemma for investors. You can try to find the "needles in the haystack" or you can simply buy the whole haystack (passive index investing).

At Variant Perception, we take a third approach: Remove the hay.

Improvement by Subtraction

Most investors focus on "Improvement by Addition." They scour the market for the next hot theme, trying to add winners to their portfolio.

We are fans of "Improvement by Subtraction". If the majority of stocks end up contributing negatively to returns anyway, then we should identify why and look to avoid these stocks.

This is where Quality comes in.

When we rank stocks by quality, we find that the lowest quality stocks tend to consistently underperform. Therefore by avoiding these stocks, investors have a path to outperformance.

Defining Quality: The Three Pillars

What does a "Quality" company look like? We define Quality across three dimensions:

- Profitability: Does the business actually make money? We look for businesses with high Gross Profit over Assets and High Cashflow generation.

- Sustainable Growth: Is the growth real or a sugar high? We prefer predictable, recurring revenue streams and are cautious of volatile, "lumpy" growth that often disappears when the economic cycle turns.

- Safety: True quality is tested in a crisis. We avoid companies that rely on cheap debt or aggressive accounting to fuel growth. A reasonable Net Debt-to-EBITDA ratio ensures resilience, while it is important to scrutinize accruals to ensure reported profits are backed by actual cash flow.

Businesses that can self-fund their growth without endangering their solvency offer compounding and resilience. Conversely, businesses that suffer from the deadly combination of eroding fundamentals, shrinking markets, and high financial risk are often value traps - "cheap, but melting ice cubes."

Why doesn't everyone do this?

If quality is so obvious, why isn't everyone doing it? Because it requires uncommon patience.

During speculative manias, low quality stocks can temporarily outperform. It is psychologically painful to watch unprofitable companies skyrocket while your portfolio is only growing steadily. Many investors capitulate and chase the momentum. This is the "Boring Penalty", the price to pay for long-term outperformance.

Additionally, true quality investing is not simply buying good companies at any price. Even a perfect business can become a poor investment if bought at 100x earnings. Our process demands that we never overpay for quality.

The Takeaway

Most investors try to win by finding the next needle in the haystack. We simply remove the hay. By systematically avoiding low-quality companies, we aim to capture the market's compounding potential while tilting the mathematical odds in your favor. Quality isn't just a factor; it is the art of winning by not losing.

Other Insights

Practical insights on allocation, diversification, and risk tolerance—combining behavioral, liquidity, and structural perspectives.

Stay Connected

Our research is built for investors who need timely, repeatable insights.