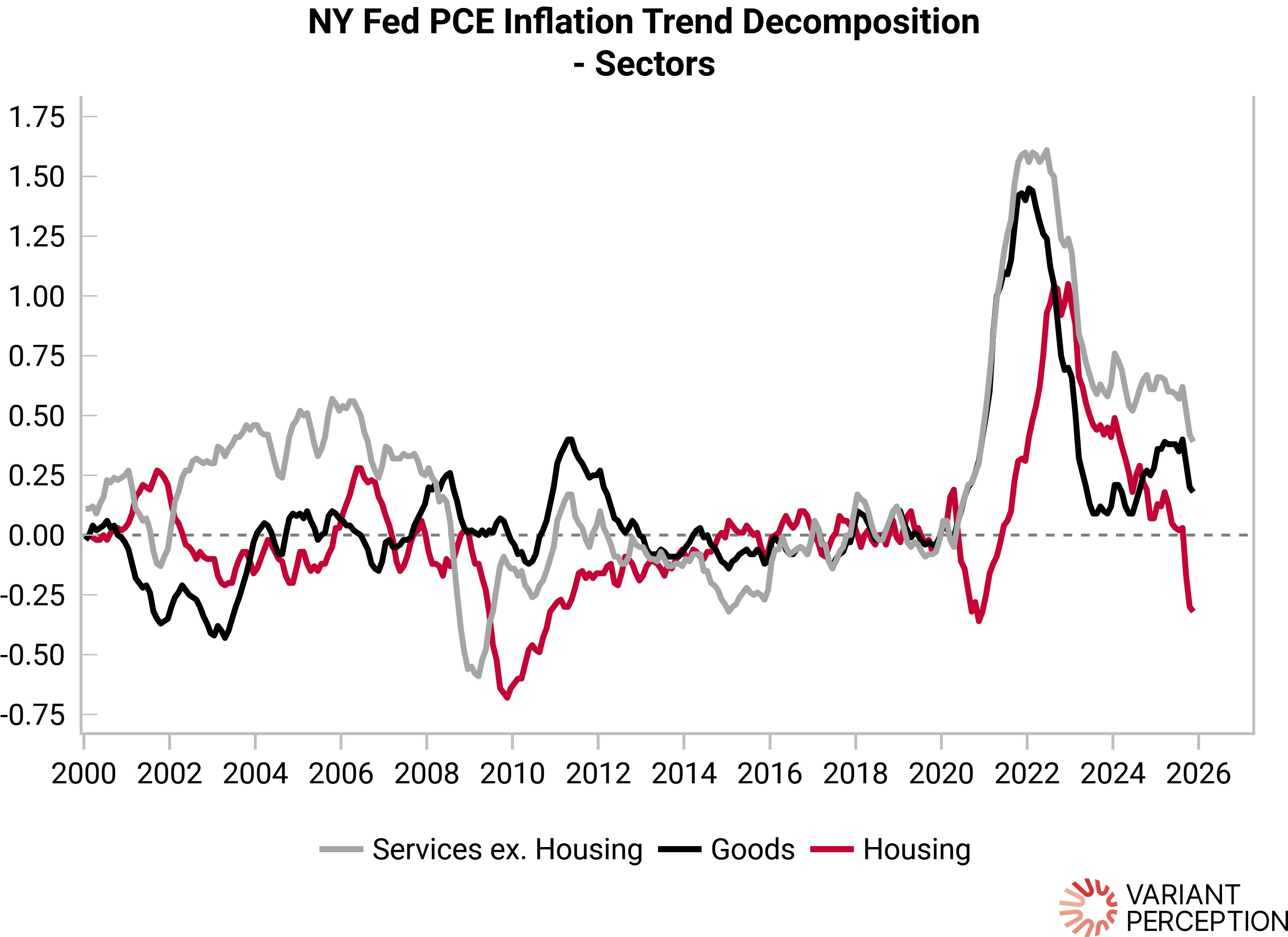

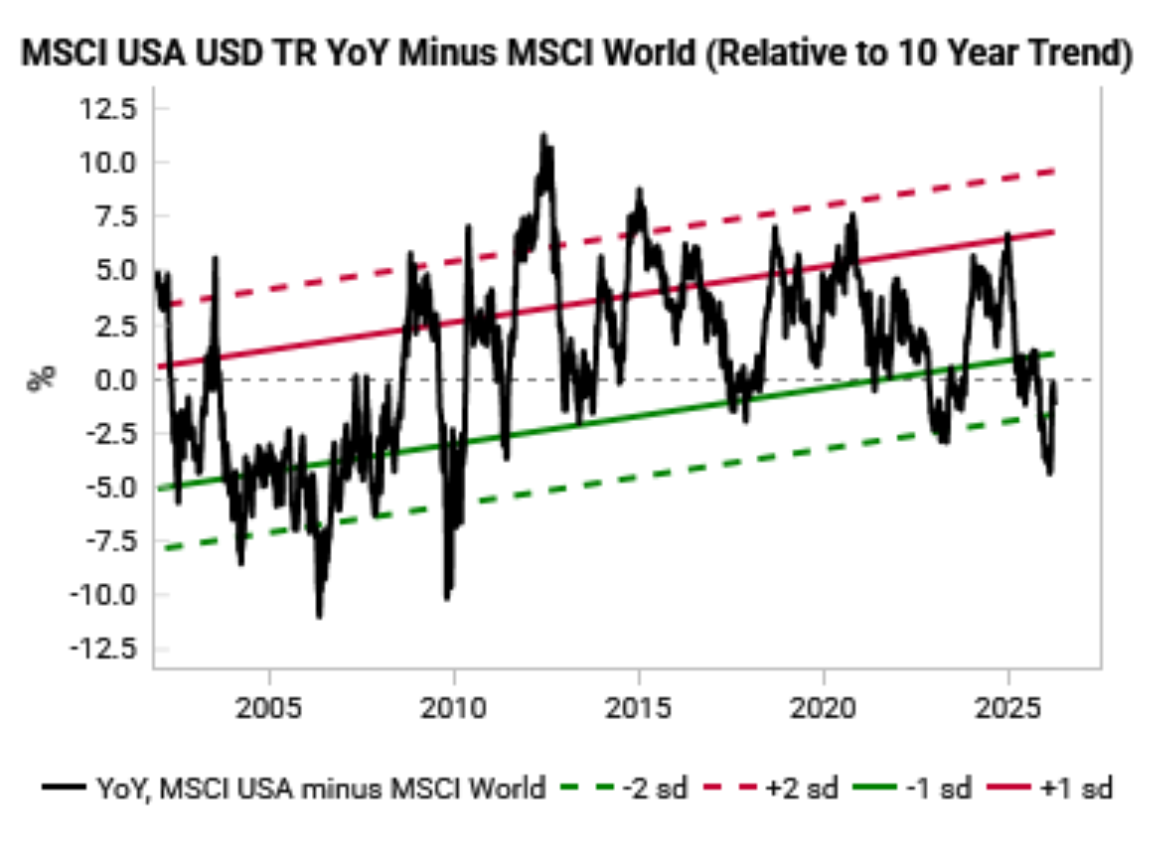

Chart of the Week

***

Research This Week

LEIs steady, incoming data marginally worse - Feb. G3 LIW | [Watch Discussion]

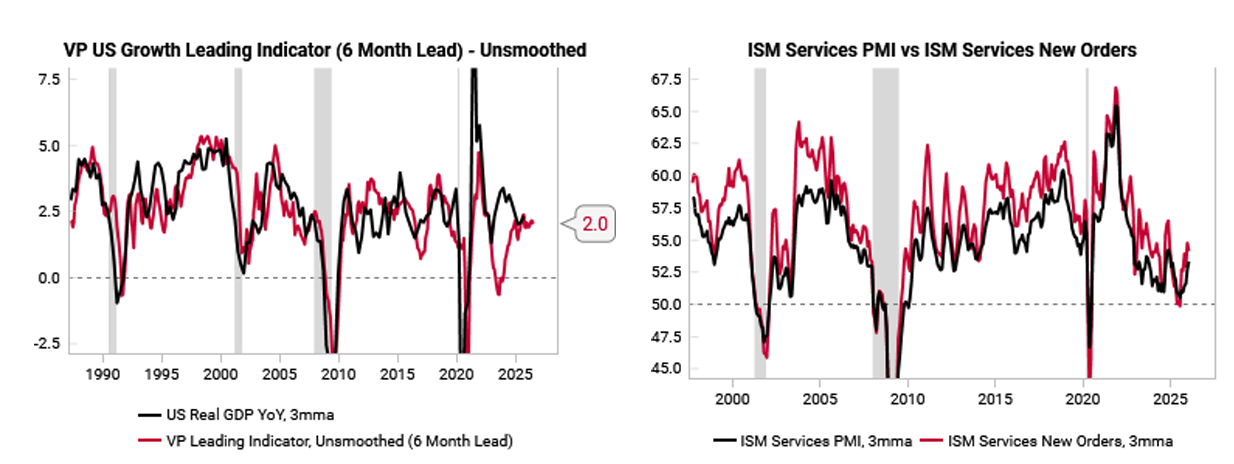

- US: Leading indicators are steady overall, but incoming data have worsened relative to a month ago. On balance, dissaving from the government and household sectors, along with a pick up in AI-driven capex, are supportive of growth.

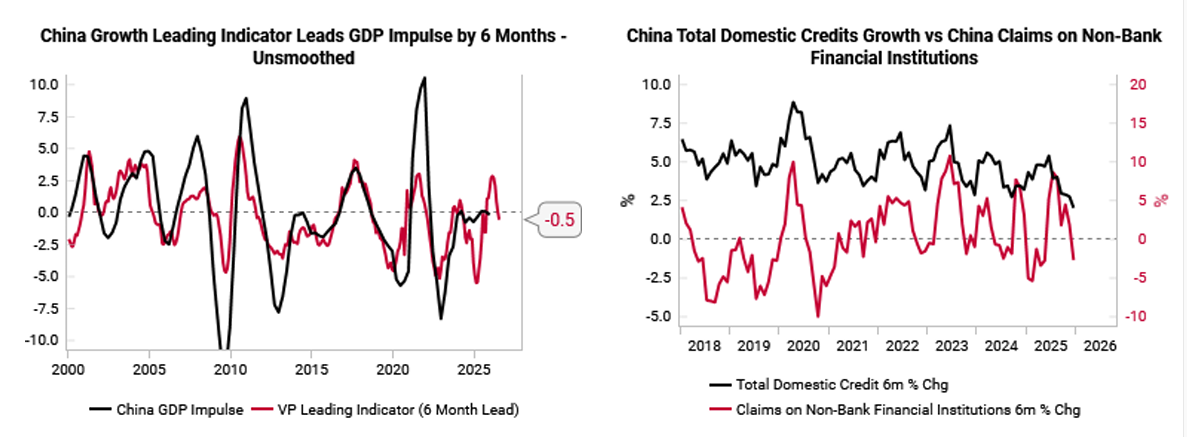

- China: Growth and liquidity have worsened, even as the structural weakness in the housing and consumer sectors persist.

- Eurozone: Growth leading indicators are recovering, but structural headwinds suggest the balance of risks for EUR is still to the downside.

***

US

- Growth: Leading indicators remain steady

- Consumer: Consumption resilient in aggregate, credit stress bubbling up outside banks

- Labor: Base case remains jobless growth

- Inflation: Set to stay above target, but disinflationary impulses are building

China

- Growth: Leading indicator turns down, liquidity deteriorates

- RMB: Struggling to get excited about RMB strength

Eurozone

- Growth: Too late to embrace optimism, too early to feel structural headwinds

- EUR: Balance of risks for EUR still to the downside

***

Other Insights

Practical insights on allocation, diversification, and risk tolerance—combining behavioral, liquidity, and structural perspectives.

Contact Us

Stay Connected

Our research is built for investors who need timely, repeatable insights.