Chart of the week

***

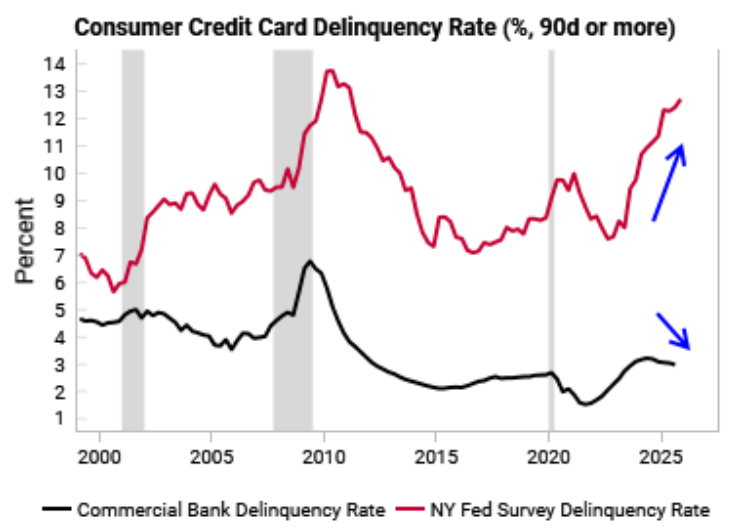

Klarna $KLAR shares recently slid.

In this cycle, US commercial banks have been reporting much lower delinquencies than the equifax data. It suggests that vulnerable consumer credit has shifted from traditional banks into "other" forms of financing like Buy Now Pay Later etc.

We laid this out in our February G3 LIW report last week.

***

Research This Week

Country-specific drivers coming to the fore - Feb. EM/DM LIW | [Watch Discussion]

- Our 2026 EM/DM Themes pointed out that country-specific factors would matter more this year given the overall benign macro backdrop. This is now more noticeable with diverging growth, policy, and inflation outlooks among different economies.

- Main DM outliers are the UK (stagflationary outlook) and Australia (inflation upside). In EM, we still like the macro setups in Brazil and Indonesia, which should benefit equities, while Korean inflation pressures keep us bullish on the KRW.

- There is no change to our positioning since our update on Feb 5 th. See Macro Ideas for the full list of our current ideas.

***

***

Notes

DM

- UK: More weak data amid stubborn inflation, stick with BoE cutting more later

- Japan: “Impossible trinity” dynamics persist, global drop in yields offer reprieve for now

- Australia: Resilient growth underpinned by housing, inflation remains sticky

- Switzerland: Large current account surplus + no inflation => CHF still biased stronger

EM

- Brazil: Inflation falling and growth improving => stay bullish equities and bonds

- Mexico: MXN still vulnerable ahead of USMCA

- Indonesia: MSCI threat a catalyst for positive reforms, macro outlook still benign

- South Korea: Inflation risks and Bank of Korea focus on FX is bullish KRW

Other Insights

Practical insights on allocation, diversification, and risk tolerance—combining behavioral, liquidity, and structural perspectives.

Contact Us

Stay Connected

Our research is built for investors who need timely, repeatable insights.