***

Second order impacts - Apr. G3 Leading Indicator Watch - April 13, 2026

- Had you been told at the end of March that the Chinese supported an Iranian ceasefire and that Vice President JD Vance would be meeting in person with senior Iranian officials, these events would likely be taken as tangible evidence that we are nearer the end of the crisis than the beginning.

- Our roadmap remains that the Ras Laffan strikes marked peak uncertainty on the Iran conflict (link). There is a (messy) path to de-escalation. It is rational for markets to look through short-term disruptions as this is a reflection of the old adage that “markets stop panicking when policymakers start panicking.”

- The question now is what second-order impacts are there for 2H26. The main risk is the potential reduction in excess liquidity from less policy easing and more inflation, just as major IPOs like SpaceX and potentially Anthropic are coming to market.

***

Notes

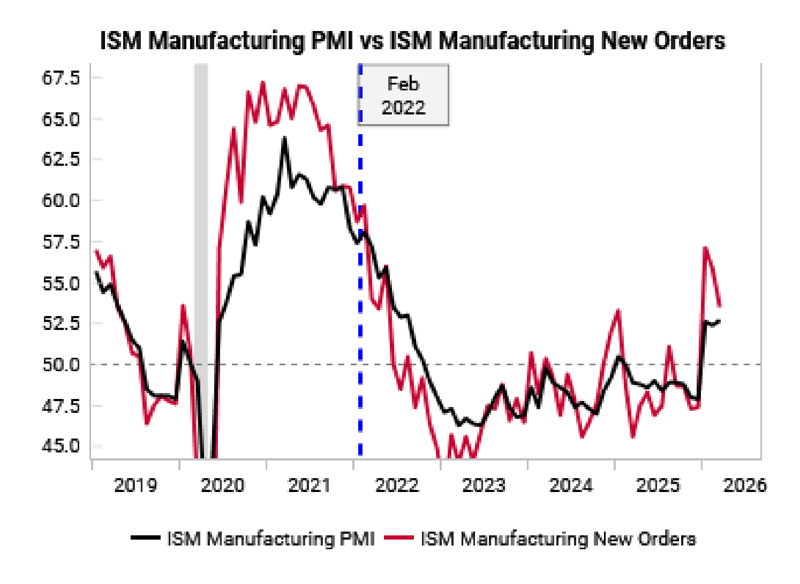

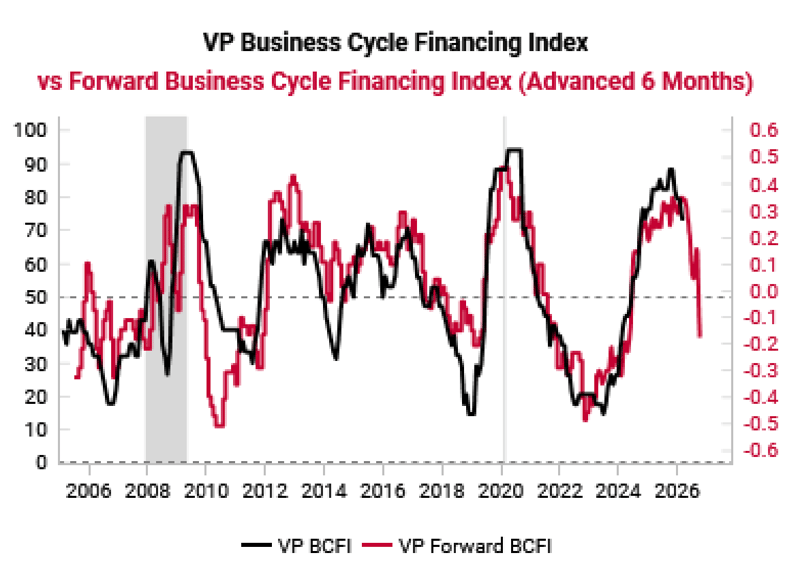

- Global: Keeping an eye on excess liquidity risks in 2H26

- US Growth resilient in face of Iran conflict

- US Inflation to settle above 3.5%, not enough for hikes, but delays cuts

- China growth: Muted outlook, Iran conflict snuffing out last bottoming signs

- China Inflation: The bad kind, China no longer exporting deflation

- Eurozone Growth: Worst starting conditions within G3, LEIs rolling over

- Eurozone Inflation: ECB is stuck, risk of 2011-style policy error

Other Insights

Practical insights on allocation, diversification, and risk tolerance—combining behavioral, liquidity, and structural perspectives.

.webp)

Contact Us

Stay Connected

Our research is built for investors who need timely, repeatable insights.